Possible Changes to IDD Delayed Until Further EIOPA Review

The Insurance Distribution Directive 2016/97 (“IDD”) regulates the way in which insurance products are designed and sold across the EU. IDD was transposed into Irish law by the European Union (Insurance Distribution) Regulations 2018 (S.I. No. 229 of 2018).

In January 2022 the European Insurance and Occupational Pensions Authority (“EIOPA”) published a report on the application of the IDD and its impact on the EU insurance market.

While IDD came into operation in October 2018, EIOPA notes that in some Member States its transposition was delayed and this makes it difficult to draw robust conclusions at this early stage. Additionally, the EIOPA report highlights factors such as COVID-19 and digitalisation as having affected the market and therefore they plan to reassess the impact of IDD in two years’ time before proposing any major changes to the current legal framework.

The EIOPA report examines the impact of IDD under three main headings:

- the changes in the EU insurance distribution market,

- the impact of the new regulatory framework, and

- the impact of the new supervisory framework.

(i) Changes in EU insurance distribution market

The report indicates that within the EU the number of intermediaries over the period 2016 - 2020 has largely decreased. It also notes that bancassurers have played a significant role in the distribution of life insurance whereas other intermediaries have distributed the majority of non-life insurance contracts. EIOPA found that online sales seem to be increasing on a yearly basis, a trend that was further enhanced by the impact of the COVID-19 pandemic.

(ii) Impact of the new regulatory framework

EIOPA states that some trade associations have reported a positive impact of the IDD on how insurance is distributed to consumers, citing a reduction in the number of customer complaints. However, consumer associations have highlighted, in particular, problematic practices in relation to the sale of unit-linked life insurance products and mortgage and consumer credit protection policies.

The Report notes that instances of lack of training of insurance distributors need to be addressed, especially with regard to certain type of insurance-based investment products which are not easily understandable to consumers.

EIOPA further identified two areas where the opportunities presented by digitalisation and new distribution models over the past three years could not be fully reaped. This, it said was due to the legal framework not having sufficiently adapted the form and timing of disclosures to reflect the digital environment, and was also due to the legal framework not having sufficiently enabled firms to address the opportunities and risks presented by digital platforms and artificial intelligence.

(iii) Impact of the new supervisory framework

Oversight of the IDD framework is provided by National Competent Authorities (“NCA”) – in Ireland this is the Central Bank of Ireland.

EIOPA found that the level of resources dedicated to conduct of business supervision had increased moderately between 2018 and 2021. Nevertheless, EIOPA's oversight work has illustrated that not all NCAs have sufficient tools to carry out effective conduct of business supervision.

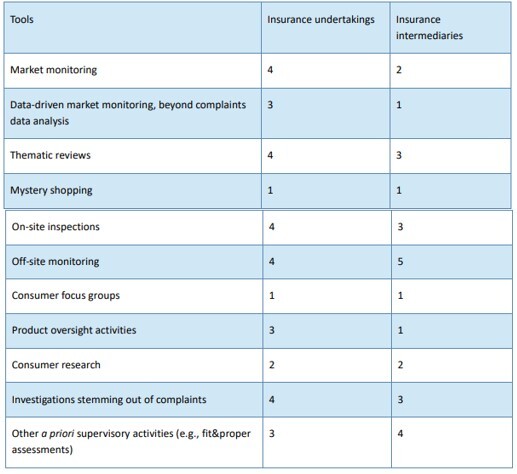

Several NCAs indicated that they would like to adopt mystery shopping activities. According to the information provided by NCAs, the most common supervisory tools used by them to monitor the implementation of the IDD are on-site inspections and off-site monitoring.

In response to an EIOPA survey the CBI has indicated, as shown in the Table below, the most common supervisory tools that it uses to monitor the IDD implementation (1 = least common, 5 = most common):

With regard to other supervisory activities, NCAs mentioned that they have adopted the following supervisory tools in the course of the implementation of the IDD:

- Assessment of professional knowledge and continuing professional training and development, extension of fitness and probity requirements to the management and owners of insurance intermediaries;

- Supervisory letters addressed to insurance distributors;

- Supervision of compliance with the IPID;

- Meeting with stakeholders

While the EIOPA report notes that the number of intermediaries with the ability to passport increased steadily over recent years, there is room to further enhance cross-border trade. EIOPA notes that “the insurance distribution market in the EU remains diverse and widely fragmented” and cites the fact that there is a “wide variety of national distribution channels, registration requirements and reporting frameworks across the EU”.

IDD is just one piece of the Single Market jigsaw. If the EU single market for insurance is to become a reality, many more pieces need to be put in place. Unsurprisingly, some stakeholders referenced the persistence of well-known obstacles to conducting cross-border business, which include the lack of a harmonised European insurance contract law, social security law and tax law.

While firms across the EU can breathe a sigh of relief that no changes will be made to IDD at this point, it is expected that EIOPA will be proposing changes when it publishes its next review in early 2024.